"In Investing, what is comfortable is rarely profitable." — Robert Arnott

Debt mutual funds receive little to no attention from retail investors. The most important reason being the difference in returns that debt mutual funds and equity mutual funds generate.

The debt market consists of various instruments that facilitate the buying and selling of loans in exchange for interest. Debt mutual funds offer a spectrum of solutions for a wide range of investment needs, risk appetite, and investment tenures.

Equity is easy to understand. But debt is complicated for some. It simply is a loan. Debt, bond, debentures all these terms imply that the investor is lending money or giving a loan to an entity. So, debt is a loan that you lend to an entity and the entity pays you interest on the loan (principal) it has borrowed from you.

What is a Debt Mutual Fund?

A debt mutual fund invests in fixed-interest generating instruments like corporate bonds, government securities, treasury bills, and other money market instruments. As compared to equity mutual funds, they bear a very low risk as they remain unaffected from the market volatility and the issuer pre-decides the interest rate as well as the maturity period. Hence, as an investor, you know the return you will be getting for investing in it.

How do Debt Funds work?

(Credit quality refers to the trustworthiness of the borrowing entity. A number of firms specialize in assigning credit ratings to borrowing entities. Some names are ICRA, CARE, etc. They evaluate companies based on their financials, management, etc, and assign a rating that makes things simple for prospective lenders.)

Based on their credit rating, they invest in a variety of securities. The fund manager of a debt fund ensures that he invests in high rated credit instruments. A higher credit rating means that the entity is more likely to pay interest on the debt security regularly as well as pay back the principal upon maturity. Debt funds that invest in higher-rated securities are less volatile when compared to that of low-rated securities.

Who should invest in Debt Funds?

Debt funds earn decent returns as they invest across all classes of securities. However returns are not guaranteed, but they are usually in the desired range. They are meant for investors looking for lower risk.

They are also suitable for people with both short-term and medium-term investment plans. Short-term ranges from three months to one year, while medium-term ranges from three years to five years.

Short-term debt funds( 3 to 12 months)- Liquid funds are ideal for short term investors, rather than keeping your funds in a regular savings account. They offer a return of around 7% to 9%. Also offers liquidity to meet emergency situations.

Medium-term debt funds( 3 to 5 years)- Many opt for Bank Fixed Deposits when thinking of investing in a low-risk instrument for 5 years. When compared to 5-year bank FDs, debt funds like dynamic bond funds offer higher returns. There are also monthly income plans If you are looking to earn a regular income from your investments.

Types of Debt Funds

To suit different types of investors, there are many types of debt mutual funds. They are classified based on the maturity period of the debt funds. They are as follows,

Liquid Funds

They invest in debt instruments like commercial papers, certificates of deposits, treasury bills, etc with a maturity of not more than 91 days. These funds are better alternatives to savings bank accounts as they provide similar liquidity with higher returns.

Income Funds

The average maturity of income funds is around five to six years. They invest predominantly in debt securities with extended maturities.

Money Market Fund

Money Market Funds invest in money market instruments like commercial papers (CPs), certificates of deposits (CDs), treasury bills (T-Bill), etc., having a maturity of less than 1 year. These funds are suitable for investors with moderately low-risk appetites. Investors should have 1 – 2 year investment tenures for these funds.

Dynamic Bond Fund

They usually have high sensitivity to interest rate changes. The fund manager keeps changing portfolio composition as per the fluctuating interest rate regime. They have different average maturity periods as these funds take interest rate calls and invest in instruments of longer and as well as shorter maturities.

Corporate Bond Fund

They invest at least 80% of their total assets in the highest-rated instruments. The highest rating given by agencies like CRISIL and ICRA for corporate bonds is AAA and for short-term instruments is A1. These are good for investing in high-quality corporate bonds.

Gilt Fund

These funds invest at least 80% of their assets under management in Government Securities. Hence these funds have very low credit risk. However, these funds have high sensitivity to interest rate changes.

Credit Risk Fund

They invest at least 65% of their total assets in instruments that are rated below the highest rating. They give higher yields but also have higher credit risks. Investors should understand the risks in these funds before investing.

Banking and PSU Fund

These invest at least 80% of its total assets in debt securities of PSUs and banks.

Overnight Funds

These debt funds invest in fixed income instruments which mature overnight. These instruments have virtually no interest rate risk and also have no credit risk. These are the safest debt funds but their yield is usually also the lowest.

Short-Term and Ultra Short-Term Debt Funds

These are debt funds that invest in instruments with shorter maturities, ranging from one year to three years. Short-term funds are ideal for conservative investors as these funds are not affected much by interest rate movements.

Long duration Fund

These invest in debt and money market instruments such that the Macaulay Duration of the fund is greater than 7 years. (In simplified terms, Macaulay Duration is the interest rate sensitivity of a fixed income instrument).

Fixed Maturity Plans

These funds invest in fixed income securities such as corporate bonds and government securities. All FMPs have a fixed horizon for which your money will be locked-in. This horizon can be in months or years. However, you can invest only during the initial offer period.

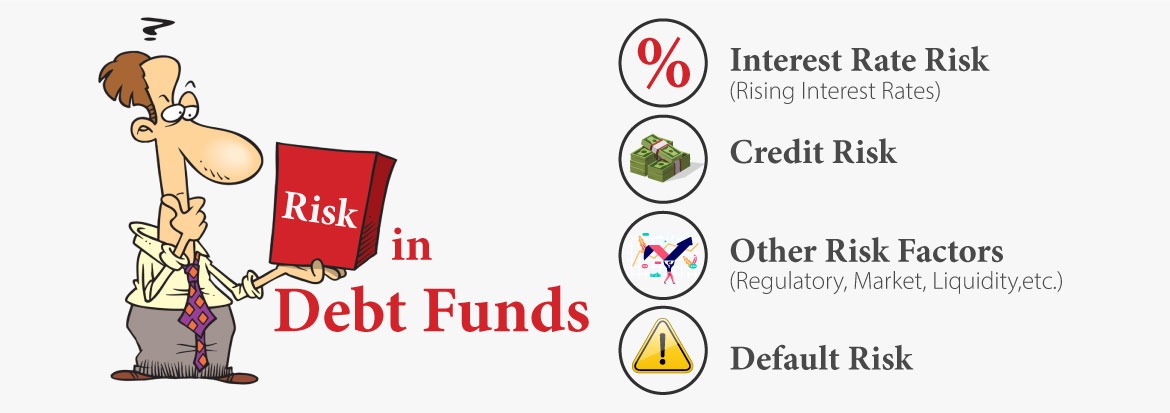

Risk Factors

Liquidity Risks- Mutual funds should be liquid in nature so that when an investor needs to sell his units the bonds can be sold. There are some debt mutual funds which are not that liquid in the secondary market hence getting the money back at the time of need can be very challenging.

Credit Risk- The kind of risk associated with the credit quality of a bond is not only associated with the default of the bond rather there is also a possibility of a downgrade or upgrade of the bond rating.

Interest Rate Risk- Interest rate risk measures the price movement of bonds with respect to change in interest rates. Other Factors to consider

Returns

The yields of many of these instruments are usually higher than bank FD interest rates of similar maturities. In addition to higher yields, since these instruments are traded in the market, you can benefit from price appreciation. Also one should keep in mind that it may not be guaranteed returns.

Expense

Fund managers charge a fee to manage your money called an expense ratio. The upper limit of expense ratio to be no more than 2.25% of the overall assets. Considering the lower returns generated by debt funds as compared to equity funds, a long-term holding period would help in recovering the money paid as the expense ratio.

Capital Gains Tax

Based on the time you stay invested in a debt fund, the rate of taxation is calculated.- If the units of the funds are sold within 3 years from the date of purchase then capital gains arising out of the sale of units will be treated as short-term capital gains(STCG) for tax purposes. STCG is added to your income and taxed according to your income tax slab rate.

- If units of the funds are sold after 3 years from the date of purchase then capital gains arising out of the sale of units will be treated as long-term capital gains(LTCG) for tax purposes. LTCG is taxed at 20% after allowing for indexation benefits.

Investment Horizon

Based on your investment objective and capital, you can select from different types of debt mutual funds. Some opt for debt funds to create wealth for the long term and some opt for regular income. So based on your objective, risk appetite, and financial obligations, you can decide.